When Beneficiaries Change Without Notice: Lessons from the Fifth Circuit's Entergy Case

A Fifth Circuit case shows how outdated 401(k) beneficiary forms can cost millions. Learn the rules, risks, & steps to protect your retirement legacy.

Introduction: What Opened My Eyes

A few weeks ago, I came across a case that made me pause. It's not every day you hear about adult kids losing out on a $3million 401(k) because of a legal technicality. That's exactly what happened inLeBoeuf. Entergy—a case decided by the Fifth Circuit on May 1, 2025. If you think your beneficiary forms are "set it and forget it," this one might make you rethink everything.

Here's the nutshell: a retirement plan participant had named his four children as beneficiaries. After he remarried, he never updated the form. The plan mailed quarterly statements listing the kids but didn't warn him that marriage voids prior beneficiary designations without spousal consent. When he passed in 2021, the plan paid out to his new wife under ERISA rules—and the kids got nothing. They sued Entergy and its advisers, but ultimately lost, because the Fifth Circuit found they weren't owed any additional warning beyond what the plan documents spelled out.

Why this matters to you (or your clients): it highlights how carefully retirement plans are structured for beneficiary decisions—and how important it is to stay on top of yours. Let's unpack what happened, break down the legal reasoning, and give you practical takeaways.

How the Facts Unfolded

Meet the Parties

- Alvin Martinez worked for Entergy (and its predecessors) from 1967 to 2003.

- In 2010, after his first wife passed, he named his four adult children as beneficiaries of his 401(k).

- The form clearly stated: "If you remarry, your old beneficiary designation is automatically revoked unless your new spouse signs a waiver." Reinhart Law+8masudafunai.com+8NAPA Net+8Your ERISA Watch®+1Roberts Disability Law, P.C.+1

Re-Marriage and Silence

- In 2014, he remarried Kathleen Mire.

- He never changed the beneficiary form, nor did his new spouse sign the required waiver.

- Even though the plan sent quarterly statements showing the kids as beneficiaries, none included a reminder of the marriage-waiver rule. Norton Rose Fulbright+6Thomson Reuters Tax+6Roberts Disability Law, P.C.+6CaseMine

An Unexpected Outcome

- Martinez died unexpectedly in 2021, leaving ~$3 million in his 401(k).

- Under ERISA § 1055(a)(2), remarriage invalidated any previous beneficiary designation unless a waiver was in place. This meant the legal spouse—Mire—automatically became the beneficiary. Barclay Damon+9CaseMine+9Roberts Disability Law, P.C.+9

- Entergy's Employee Benefits Committee and the plan trustee, T. Rowe Price, paid Mire—not the children.

Legal Challenge

The children sued, claiming

- Breach of fiduciary duty—they argued Entergy, the Committee, and trustee misled the participant by continuing to list the kids as beneficiaries without alerting him of the rule.

- They said this constituted a material misrepresentation or omission under ERISA.

This was dismissed in district court and the Fifth Circuit affirmed on May 1, 2025 Reinhart Law+9Roberts Disability Law, P.C.+9CaseMine+9CaseMine+1Bloomberg Law News+1Thomson Reuters Tax.

Understanding the Law & LegalAnalysis

Who Is a Fiduciary Under ERISA?

ERISA only makes certain parties"fiduciaries"—those with authority or power over plan management, assets, or participant communications. Courts have been very clear:

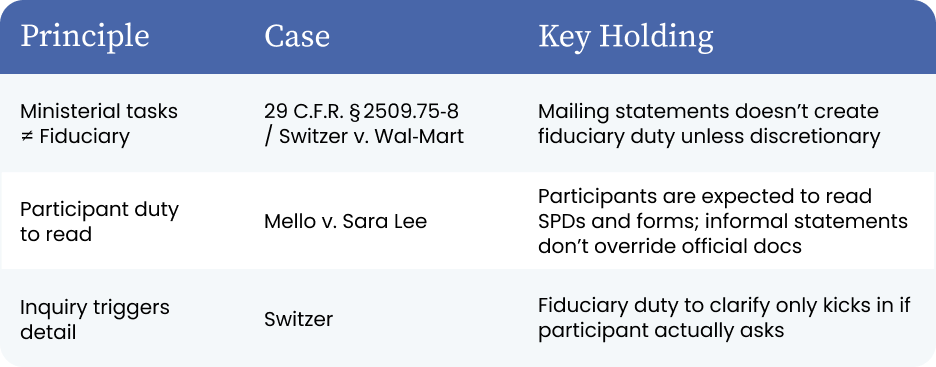

- Entergy: Not a fiduciary here—its administrative role didn't give it discretion or authority Bloomberg Law News+11Roberts Disability Law, P.C.+11CaseMine+11CaseMine

- T. Rowe Price: They only handled ministerial communications (mailing statements), which legal precedent holds don't create fiduciary responsibility Your ERISA Watch®+3Roberts Disability Law, P.C.+3CaseMine+3

- Employee Benefits Committee: It is a fiduciary, but only the Committee, because it has discretionary control under the plan. CaseMine+2Roberts Disability Law, P.C.+2Your ERISA Watch®+2

Was There a Breach?

Under ERISA, for a fiduciary to haveviolated its duty, two things are require

- A material misrepresentation or omission in plan communications

- Detrimental reliance by the participant, meaning he relied on the misleading info to his detriment

In this case

- Plan language, SPDs, and the beneficiary form all clearly warned that remarriage voided previous designations absent spousal waiverCaseMine+5Roberts Disability Law, P.C.+5Thomson Reuters Tax+5

- The Fifth Circuit ruled that sending quarterly statements listing old beneficiaries didn't override official plan communications

- Participants have a continuous duty to understand the plan; fiduciaries don't have to re-teach plan rules proactively, it only kicks in if a participant asks for info ESG Dive+15CaseMine+15Your ERISA Watch®+15

So even though the statements could have been misleading, legally they weren't enough to show a breach.

Real-Life Takeaway: What This Means

Your Forms Matter, Big Time

Beneficiary designations are not"set-and-forget." You must match them to your current life situation

- Get married or divorced? Change forms.

- Add grandkids? Review.

- Remarriage? Especially important, make sure your new spouse signs waivers if needed.

Read the Plan, Not Just the Statements

Statements are for visibility, but the actual rulebooks are the Plan Document, SPDs, and beneficiary forms. You can't rely only on info on the periodic statements.

No One's Watching Like You Are

Plans aren't responsible for reminding you unless you ask. Stay on top of your own retirement, your financial future depends on it.

Law Favors Precision

Since ERISA requires actions "solelyin accordance with plan documents," courts give every benefit of the doubtto what's written in official documents, not what might be casually communicated. Reinhart Law+2Roberts Disability Law, P.C.+2NAPA Net+2NAPA Net+1Roberts Disability Law, P.C.+1Fifth Circuit Court+8Thomson Reuters Tax+8masudafunai.com+8Barclay Damon+1ESG Dive+1

Case Law Context

This Fifth Circuit case reinforces a few key ERISA rulings:

What I Usually Tell Clients

When the Entergy case first came out, I told a longtime client this:

You can't assume your plan is raising red flags on life changes, it probably isn't. It's on you.

Here's what I recommend:

- Annually review your beneficiary designations for all retirement and investment accounts

- Update immediately after any change in marital status, family structure, or estate plan.

- Keep copies of your signed forms and SPDs, if a dispute hits, documentation wins.

- If you're remarrying, don't skip the spousal waiver. Otherwise, ERISA steps in automatically, and against your kids.

- Ask questions. If you get a statement that surprises you (e.g. too many named kids?), reach out for clarification.

What You Should Do Now

- Pull your latest beneficiary forms.

- Check your SPDs and plan documents for remarriage rules

- Cross‑check your spouse's signature (if applicable).

- Document any updates and note the date.

- Schedule a reminder in your calendar to review annually, or when life changes.

Final Thoughts: Planning Lesson of the Day

The Entergy case isn't just a legal oddity, it's a real-world warning. It reminds us that life changes matter and legal precision matters more.

If you don't keep retirement plan forms current:

- ERISA kicks in with rules that may go against your wishes

- Statements and signals from plans aren't enough to protect your legacy

- Beneficiary mistakes can be costly for your loved ones

You've worked hard to build retirement savings. A few minutes now to check your paperwork can save hundreds ofthousands, or more, down the road.

Want help diving into your plans, or setting up that annual checklist? I'd be glad to support you or your clients in making sure all the boxes are checked and your wishes are front-and-center.

Powering Your Retirement is a Registered Investment Advisor. Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. The information contained in this material is intended to provide general information about Powering Your Retirement and its services. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement.

You May Also Like,

Here are some must-read blogs you don’t want to miss! Get expert tips on retirement benefits, 401(k) management, and more. Stay in the know and make the most of your retirement planning!

Are You Ready for Retirement?

Book your free, no-strings-attached assessment—a stress-free process where we’ll tell you the exact amount you need to retire, when you want to!